MakerDao

A deep dive into one of the oldest dAPPs

Maker Investment Thesis

This article will first explore the stablecoin sector as a whole, then introduce MakerDao in three stages, the past (V1), present (V2), and future (V3) and explain why we like it as an investment.

1 Stablecoins

Crypto suffers from large magnitudes of volatility due to its infancy, illiquidity, and speculative nature. The first stablecoin was introduced in 2014 as a way to mitigate this volatility and since then the fiat backed stable coins have become an important part of the ecosystem. They create a more efficient, stable, and accessible experience to all. Popular use cases include:

Store of Value: Reduces overall volatility of digital portfolios. Without stable coins all, crypto wallets would suffer from extreme volatility.

Remittances: Sending money is trivial, magnitudes faster, more efficient, and accessible to all without fees or paperwork.

Trading: Allows trading on exchanges without access to traditional banking. Instead of settling all pairs in USD, exchanges can settle in stablecoins like USDT.

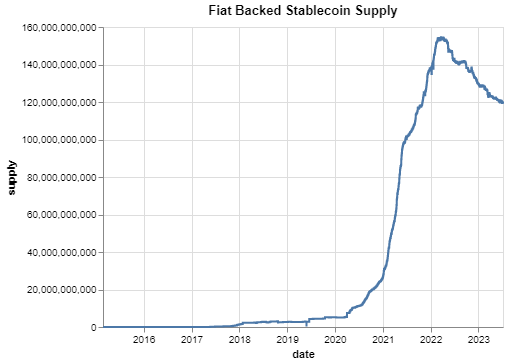

Below is a chart showing the total market cap of the largest six fiat backed stablecoins1. At the zenith of the last bullrun, the stablecoins reached a peak of around 160 billion and now sit at a little over 120 billion, which is over 10% of the entire crypto market cap. Around 70% of the supply is in USDT while another 25% is in USDC.

1.1 Profitability

Stablecoins are one of the few sectors in the crypto ecosystem that make profit due the dollars being put in yield bearing assets similar to how a bank would treat deposits. Looking at the public balance sheet Tether published, we see they have around 81.8B in assets and 79.4B in liabilities (USDT mcap) and made 1.48B2 in just the first quarter alone. They do this by rehypothecating their consumer holdings into safe investments like short term treasury bills which can clip north of 5% in today's environment. For reference, placing 80B in short term tbills3 would net Tether around 4.5B in profits.

For a metric of how unusually lucrative that is, Coinbase, the second-largest spot exchange by volume, made only 736m in total revenue and actually lost money after expenses. A lot of crypto companies are privately held and have limited public information, but we would venture that Tether (and by extension Circle, the parent company behind USDC) generate more revenues than the rest of the crypto industry combined ex-Binance. Unfortunately for the general public, it is currently impossible to invest in either Tether (USDT) or Circle (USDC) as they are private companies with no current plans to go public4.

1.2 Other Stablecoins Types

This isn't to say fiat-backed stablecoins do not have risks. Just a few months ago, USDC depegged to around $0.87 after 3.3B held at Silicon Valley Bank (SVB) was frozen due to the SVB bank run. For better or worse, the fiat-backed stablecoins are heavily reliant on external actors like the banking system. To this day the FDIC has not paid all depositors and there is still around a $1.9B hole.

Two other stablecoin types which have shot to prominence are algorithmic stablecoins and crypto-collateralized stablecoins. A popular example of an algorithmic stablecoin is UST which infamously broke peg and vaporized 20b of "notional" value in one day. Crypto-collateralized stablecoins theoretically do not have that downward spiral pressure of algorithmic stablecoins, nor are they heavily reliant on the banking system. This article will focus on the history of the most popular crypto-collateralized stablecoin issuer, MakerDao, its current role in the ecosystem, why we think it is a good current investment, and its future plans.

2 SAI: V1

Around the same time the fiat backed stablecoins were taking off, people began experimenting with other ways to back stablecoins. Enter MakerDao, one of the largest and oldest dapps in existence, focused on using cryptocurrencies (instead of fiat) to back a stablecoin. Initially, the objective was an overcollateralized decentralized stablecoin pegged solely to ETH and this prototype went live in 2017. Decentralized stablecoins provide many of the same advantages their centralized fiat backed counterparts provide, but also are trustless in nature and mitigate counterparty risk. The first version worked like this:

Jill deposits ETH into the MakerDao smart contract and then she is able to mint SAI (a stablecoin) at a 150% collateral ratio: which means depositing $150 of ETH creates (at most) 100 SAI. The smart contract then sends the SAI to Jill, records the amount of SAI given as a debt, and locks Jill's collateral until the debt is repaid.

Jill can then go and use her newly minted SAI while maintaining the ETH exposure that she deposited in the smart contract. A typical use case would be to swap the SAI for more ETH, inherently creating a levered position. In the example above, if Jill swaps all her SAI for ETH then she gets $250 of ETH exposure on just $150 ETH giving her 1.6x leverage.

In order to protect the collateral, ensure MakerDao does not take on bad debt while accruing revenue to the protocol, Jill needs to pay attention to the collateral ratio and the stability fee5 (interest rate minters pay). If the value of her ETH drops below the 150% collateral ratio, a portion of her collateral may be liquidated in order to move her back to the 150% mark (set through governance)6.

This early iteration of MakerDao greatly increased the capital efficiency of holding ETH. If Jill wants to redeem her collateral, she just "burns" the SAI she minted (and any additional interest accrued) by returning it to the smart contract which subsequently unlocks her ETH. Note the parameters which govern the MakerDao dapp like the collateral ratio and the stability fees (interest rate the minters pay) is determined by Maker Governance through the MKR token.

2.1 Product Market Fit

As we can see with the Sai supply chart, there was good traction and fit from day 1, just like its fiat backed counterparts. The supply increased to over 100m through November 2019, before MakerDao upgraded to the second iteration, marked by the red vertical line. Perhaps more telling of the traction of Sai were other crypto collateralized stablecoins that spawned like Frax, Fei, Liquity, RAI, and Alchemix; imitation is the sincerest form of flattery.

3 DAI: V2

In 2019, MakerDao upgraded to V2 which allowed multi-collateral to mint DAI, another stablecoin that essentially replaces SAI in the ecosystem. So instead of only ETH, other assets (voted on by MKR governance) could also mint DAI. Essentially, this update increased the DAI in circulation and reduced the oscillations of DAI supply based on ETH price volatility. Today, there are more than a handful of different assets which can be accepted as collateral such as popular liquid staking derivatives (stETH and rETH), wBTC, erc-20 LPs7, and real world assets (t bills) to name a few.

These next sections will describe the current state of the protocol and then will break down the various revenue streams of MakerDao.

3.1 V2 Overview

3.1.1 Dai Savings Rate

Along with multi-collateral assets, V2 has a few more notable improvements like the Dai Savings Rate (DSR) to incentivize people to hold Dai. The DSR is a baseline interest rate that any Dai holder can access by depositing their Dai into a separate DSR contract to incentivize people to hold Dai. The current DSR is 3.49%8 which can be thought of as the base “risk free”9 rate in crypto. There is no minimum deposit or withdrawal fees, the Maker Protocol is distributing some of its revenue to all DAI holders who deposit in the DSR.

3.1.2 Dai Collateral

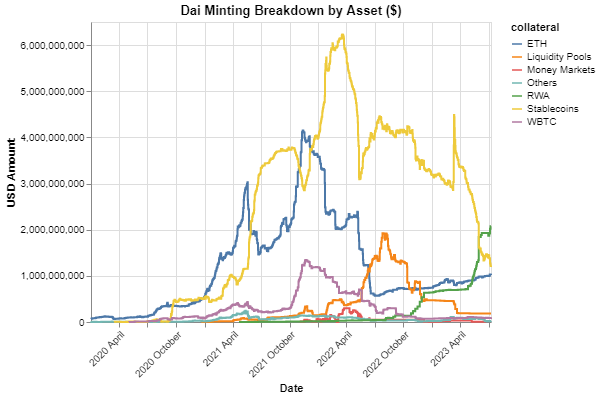

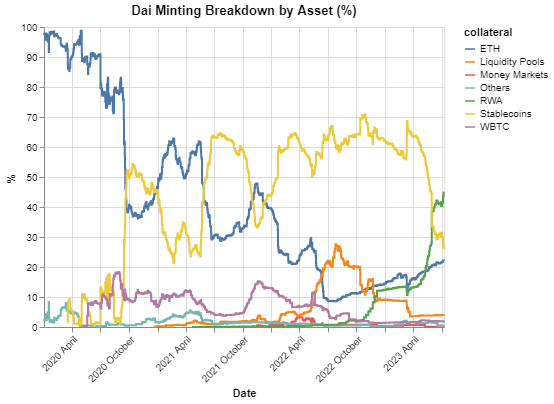

The primary method through which MakerDao earns revenue is through the stability fee income it charges depositors to mint Dai. There currently is around 9.1B in TVL in the Maker protocol and roughly 4.6 billion Dai has been minted. Initially we see that ETH was the primary method for minting, most likely a carry over from the SAI days as that was what people were comfortable with. However, in the early days, DAI was consistently over peg as people wanted DAI exposure to yield farm. MIP-21 created the Peg Stability Module (PSM), a programmatic vault which allowed stablecoins like USDC to mint DAI 1:1 for no stability fee, which is how the stablecoin explosion took off.

More recently, MIP-65 popularized real word assets to the maker protocol and the share of those has been slowly growing. In a little more than a year, the RWA portion of DAI collateral has increased from nothing to almost 50%.

3.2 V2 Profitability

3.2.1 Dai Revenue

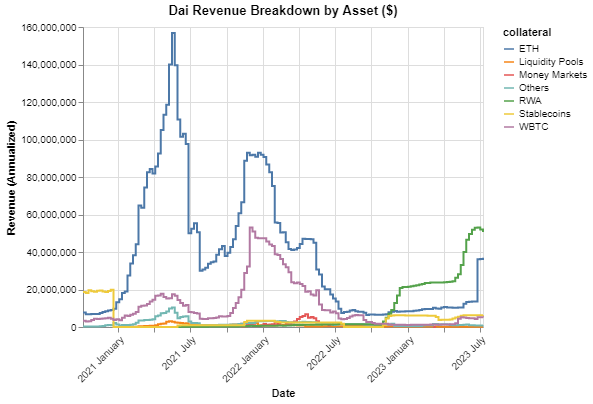

In the new multi-collateral world, the stability fee percent differs asset by asset and RWA do not have a stability fee, rather the yield is passed onto the surplus buffer which is essentially an insurance fund to take on bad debt. Below we have the breakdowns for asset class in terms of revenue. We see that initially most of the revenue was from ETH stability fees (and to a lesser extent WBTC stability fees). However from the start of this year, MakerDao has followed its fiat-backed stablecoin peers USDT and USDC by putting a large chunk into real world assets. Now more than 50% of the revenues are generated by these short-term treasury bills and other similar assets. Note that this breakdown is unrealized pnl and the future numbers are higher as the stability fee and the real world yields have both been hiked.

3.2.2 MakerDao Yield

So how much yield does MakerDao generate on its assets? Below we see a very volatile rate of annualized yield. Slowly but surely MakerDao is increasing its total yield and this is mainly a function of turning non-revenue generating stables into productive assets.

3.2.3 Expected Yield

Specifically the protocol is making around 3.79% from erc-20 stability fees or around 3.57m monthly and 42.8m annually. Then the real world assets generate roughly 6.58m or 79m annually for a total of 121.8m annually and 10.2m monthly in yield. The RWA yield is also less volatile because rates vol is lower and moves slower than prices.

3.2.4 Other Revenue

Apart from the stability fees and RWA yields, MakerDao also generates revenue from liquidations. These are not very stable pnl sources as they mainly occur when the market experiences volatility (typically on the downside). For reference, there was a monthly average of 1.37 million liquidation PNL the past year, but some months like January had 0, while others like October 2022 had over 3.92m in pnl.

Then there are PSM minting fees and flash loan fees but those are negligible when looking at the entire profitability. Adding the liquidations, we end up with an annual expected revenue of 138.24m and a monthly revenue of 11.57m. Note that outside of the fiat backed stablecoins these are extremely high numbers.

3.2.5 Expenses

To deduce overall profitability, we need to look at the expenses which include the core developer team, keepers, risk managers, lawyers, and a host of other fees to running a large decentralized organization. These numbers are ever changing with new initiatives being constantly introduced so it is very difficult to project in the future.

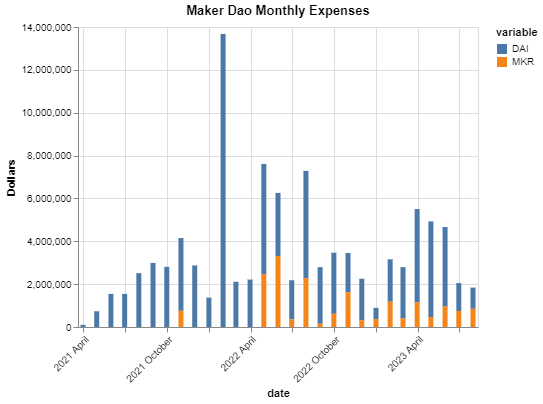

The trailing 12 month expenses hover around 38m: 29m of DAI and 9m of MKR.It is important to emphasize that there are many new spending programs that have been approved while most of the old core units are offboarding so past expenses are not a good indicator of future expenses, and some approved initiatives may not get implemented. Expenses could either rise or decline.

3.2.6 Profitability

Subtracting the revenues from the expenses, we get an annualized profit of roughly 100m. Besides the aforementioned stablecoins and a few exchanges, there really is not a more profitable dapp. The market cap of MKR is around 820 million. We (like many in crypto) have an aversion to using tradfi metrics when valuing crypto protocol and prefer to use internal KPIs, but this is a PE ratio of 8.2. At some point cheap is cheap. Even running the fully diluted market cap gives it 9.2, which is notoriously low for a tech startup. The market is valuing MakerDao like a mature bank stock whose revenues are based on yield generated and removing all future upside. For reference JPM and Citibank have similar PE ratios.

3.3 MKR Token (Immediate Catalysts)

In crypto, there are often frictions between protocol accrued value and token accrued value. Famously dYdX passes no profits/revenues back to token holders10. This is not the case with MKR. As soon as the surplus buffer is hit, the protocol previously bought back and burned MKR. A few weeks ago, smart burn was introduced which, instead of using the entire excess to buy back MKR, buys MKR with half the excess, and LPs the rest into the MKR/DAI uniswap V2 pool instead. In contrast to the burn, buying and adding liquidity will dampen the volatility of MKR on the way up and the way down, while capturing trading fees.

3.3.1 SmartBurn

The surplus buffer upper limit was recently adjusted downwards from 250m to 50m. If there is excess DAI, then it will be used in the smart burn mechanism. Given that we are at a surplus of roughly 80m11, the protocol will swap and pool 5k DAI every half an hour until the surplus buffer returns to 50m; this equates to 125 days of TWAP buys.

Note that the smart burn is not live yet and the start will initiate the beginning of Endgame, version 3 of the MakerDao protocol. This protocol owned 50/50 MKR/DAI UniV2 pool12 is called the Maker Elixir and will increase the liquidity of MKR, give it consistent buying pressure, and capture trading fees.

3.3.2 More Revenues

500m of USDC is sitting in the PSM not earning any yield. The PSM outflows have finally slowed down and Blocktower has been contracted to slowly put the USD to work and will be able to generate north of 4.5% of those assets, giving MakerDao another 22.5m in annual revenue. If rates remain stable, we suspect MakerDao will easily be making north of 150m in annual revenue before the end of the year giving it a PE ratio of 6 if the prices hold.

3.4 Issues

There are a few large issues with V2 and some of it is correlated:

MakerDAO is too complex and disorganized leading to many divisions and fractures. This in turn breeds inefficiencies

DAI supply is in a downtrend and needs to be reversed

MKR token has had no real use case other than governance and there are not enough incentives to vote on most proposals.

Part of the infamous cursed down only Defi 1.0 coin narrative

3.4.1 Governance Issues

One of the major issues with V2 is governance apathy which in turn creates a very lethargic environment, which is often contrary to its competitors. The average MIP takes over 2 months from proposal to ratification and practically no one participates in governance. Under 40 unique people vote on each action and votes typically pass with around 5-10% of the total supply. The most recent poll, which is typical, had one individual supply 88% of the voting MKR.

In the voters' defense, MakerDao is very comprehensive and to make informed decisions is basically a full time job as they need to get educated on a large swath of issues from RWA to proper liquidation parameters. However, this large lag time causes MakerDao to be inefficient and not maximize value capture. Specifically with regards to the stability fees, governance has historically been too slow to adjust the rates on both up and down moves.

3.4.2 Yield Optimization Inefficiencies

Proper yield optimization requires constant scrutiny, precise monitoring, and accurate reporting. There characteristics can not be said for many of the RWA vaults as

3.4.3 Dwindling Dai Supply

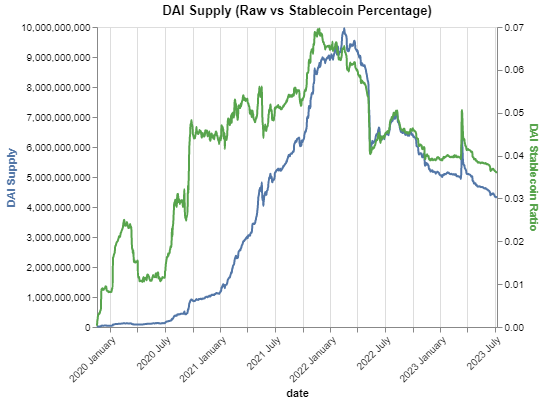

Below we have a time series plot of raw DAI supply and DAI as a percentage of the entire stablecoin market cap. During the entire runup the stability rate was far too low, rapidly increasing DAI as a percentage of the entire stablecoin market cap from 1% to around 7% at its peak, but not capturing enough revenue. The reverse happened on the way down since November 2021 as the stability rate was too high especially compared to other protocols. The DAI marketshare has dropped from that 7% peak all the way down to around 3.5% market share from 10b to slightly north of 4b in no small part because of higher fees compared to the rest of the defi borrow lend market.

It is worth noting that the remaining 4B+ DAI supply is decently sticky as a lot of the top 50 wallets are smart contracts and blackhat criminals/scammers.

3.4.4 No Real Value Accrual / Down Only Narrative

Crypto twitter at its best is a place where ideas stand on its own merit as everyone is anon. Crypto twitter at its worst is an echo chamber of shitposting where very few people have original thoughts. Enter a popular CT account DegenSpartan who has been criticizing MKR for the past four years. He addresses some valid issues but perhaps more importantly the chart agrees with him.

This is one of the ugliest charts we have seen in a while especially when examining the MKR/ETH ratio in red. The chart looks like there is a constant seller with no buying support first because of the UST crash which created negative contagion in the stablecoin space and then because for the past year and a half the MakerDao was not returning any of the value it captured to token holders13 after increasing the surplus buffer to 90m then 250m and pausing the buy back and burn program. However the smart burn has already been passed to rectify this issue.

3.5 V2 Conclusion

The current iteration of Maker is one of the most profitable protocols in all of crypto. With annual profits of 100m (and growing), the market is valuing the token price like an established bank stock with no upside or future plans. If we broke down MakerDao's cash flows and assumed no further utility to the Maker token it would be the cheapest crypto in terms of PE ratio.

That is not to say MakerDao V2 does not have its faults like inefficient revenue capture due to core governance flaws, a token that currently does not accrue value, a dwindling demand for DAI, and terrible optics from the wider crypto community in terms of sentiment and price.

All of these issues are why there is such a disconnect between fundamentals and price. A new version of MakerDao, V3 is posed to turbo charge the protocol, increase TVL, stability fees, while bringing a bunch of new value capturing methods for the MKR token and hopefully reversing the sentiment and price.

4 Endgame: V3

Rune, the founder of MakerDao, has been working on v3 for over a year. The new iteration will lead to a large change in how governance is run, tokenomics, and numerous dApps, in order to grow MakerDAO into the largest and most widely used stablecoin project within a few years. Appropriately titled Endgame, the goal of this upgrade is to create a resilient and lindy endgame state so the core of MakerDao does not change.

Specific goals are highlighted in the atlas alignment artifact and include but are not limited to:

Mass global accessibility to DAI14

Create steps to scale Maker Ecosystem in a decentralized manner

Reduce MKR concentration through new tokenomics and emissions

Reduce governance overhead for MKR holders

Perhaps more importantly it attempts to address all of the major pain points with V2.

4.1 Overview

4.1.1 subDAOs (Proficient Revenue Extraction)

To tackle the goals above, the tasks will now be reorganized into smaller, more nimble subDAOs. For instance one subDAO can hyperfocus on RWA to extract the highest yield possible. The subDAO voters will be informed on a much smaller mandate allowing them to iterate faster and have more in depth discussion and thoughts.

Each subDAO will be independently profitable, run their own businesses, and have their own SubDAO token (SDT). These new tokens will in turn be used as rewards to help specific portions of the protocol like Dai adoption and create a synergistic relationship between MakerDao and the various subDAOs.

The subDAOs allow members to specialize in certain tasks and develop specific expertise creating a more efficient and ultimately better value capture protocol. Going back to the RWA optimization example, currently vault RWA14 is making around 2.6% annualized yield on 500m. Note that US government t-bills are at 5.5% which is basically all USDC is backed by anyways so why not go directly to the source instead of giving coinbase 3%? Sure there are custody and slight diversification benefits and also a tradfi lead lag time issue where everything takes 3 business days to clear. So let's assume that we want to use Coinbase. Last month, Coinbase launched Coinbase Earn where anyone can clip 4% on yield at any size. That extra 1.4% might not seem like alot but it is an extra 7m dollars plus on 500m deposit. There are many other low hanging fruit optimizations that can be done to increase protocol revenue that each subDAO can tweak.

The Endgame will contain many groundbreaking changes, and a lot of these will stack on each other so the ordering of the upgrades is very important. Below we have a vague timeline:

Because this is a MKR investment thesis, we focus on the tokenomics portion of the pregame which prioritizes building the core products/features used in the Endgame. However we urge those interested in reading about the underlying protocol to read the forums and participate in governance.

4.2 New Tokens

There will be a token split and each MKR token will translate to 1200 New Governance Token (NGT). There will be a new chart to wash away all the down only in ETH, ew ATL shitposts. In the same vein, there will also be a New Stable Coin (NSC) that acts as a DAI wrapper. To drive initial adoption towards NSC, there will be a few yield farms, one for NGT (10m NGT or about 1.2% of total supply annually) and six for each individual subDAO (35M SDT or around 1.75% of total supply annually) that only take NSC. For the purposes of this blog, we will use MKR/NGT and DAI/NSC interchangeably.

Note that each subDAO has the same tokenomics of 230m SDT for the first year so 35m is over 15% of the first year supply. These yield farms will be a powerful marketing technique to jump start the NSC and shine a light on each individual subDAO. These farms will reverse the trend of dwindling DAI supply.

4.3 SubDAOs

There will be six subDAOs to start, two FacilitatorDAOs which specialize in operating DAO governance and four AllocatorDAOs which focus on generating use cases for NSC and allocating the various collateral assets.

Out of the 230m SDT, 200m15 are meant for farming with the following breakdown:

Similar to how MKR currently uses surplus income to buy and pool MKR, the subDAOs will do the same. The MKR elixir is a 50/50 MKR/DAI pool while each SDT will have their own elixir that is 50/50 SDT/MKR. Basically any profit in the ecosystem will buy and pool MKR giving it permanent buy pressure along with deep liquidity. It is easy to see a world where MKR is the third most liquid asset on-chain behind ETH and BTC.

4.4 Sagittarius Lockstake Engine

The final piece of the tokenomics puzzle is the Sagittarious Engine (SE) which is a MKR voter incentive and governance lockup mechanism. One of the main problems with the current iteration of MakerDao is that very few people vote and/or delegate so participation rates are abysmal (usually between 5-10%). SE locks up MKR (or NGT) for the long term, requires governance participation, and in return opens exclusive private yield farms for DAI and other subDAO tokens16.

If a depositor wants to withdraw the MKR token from SE, they incur a large 15% haircut which will be burned. This will be a very lucrative farm to encourage long term protocol alignment as initially 30% of all protocol surplus goes to SE Dai farmers. In addition, when subDAO tokens launch, 30% of all token farming will go to SE participants.

4.5 MKR Value Accrual

Unlike the worthless governance token memes, MKR will have many use cases in V3 besides governance:

Best way to farm various SDT through the SE

Maker elixir surplus buyback

subDAO elixir surplus buyback

Stake to validate new MKR chain17

5 Investment Roundup and Conclusion

In this article, we did a cursory glance at the stablecoin sector as a whole and illustrated how it is one of the only profitable sectors in crypto. Maker is the oldest and largest investable stablecoin18 and it just so happens to be really cheap by traditional value metrics which discount all future growth.

On the protocol level side, we introduced V1 and V2, while analyzing some of the shortcomings. Then we examined how V3 fixes and reverses many of the V2 issues and explained the complex new tokenomics governing V3. MakerDao is by far the largest decentralized stablecoin and the new products on V3 will only accentuate its lead. It is also the most lucrative decentralized stable coin protocol and the efficiencies created by the subDaos shall turbocharge this profitability. In my eyes these fundamental changes, along with a token redenomination (One $900 MKR turns into 1200 $0.75 NGT) and a new chart are positive catalysts for the token.

A few short term flows to note: A16Z has been unstaking MKR from governance and sending to Coinbase to sell. They have sent around 15k units and have 34k units left (19k in wallet and another 14k in governance), which we can safely assume will be sold.

Note: Nothing in the article constitutes professional and/or financial advice. Ape if you want to ape. Special shout out to SebVentures for some of the maker specific data, Blurr for putting me onto the MKR thesis, and PaperImperium for proofreading. Also thanks to the people in the MakerDao discord for answering my questions.

USDT, USDC, BUSD, USDP, TUSD, GUSD

Tether is notoriously secretive about its holdings and profits so take this number with a grain of salt. However the math checks out

Current rate is around 5.5% annualized

Circle had a SPAC attempt in 2021 that was shot down by Gary Gensler.

Take the same example, if the fee is 1% and Jill has minted 100 DAI, current her debt to the protocol would be 100 DAI. In a year her debt would be 200 DAI.

It is strongly recommended to not go full degenerate and mint the maximum available as liquidation is likely due to inherent ETH volatility

UNIV2 DAI/USDC, UNIV3 DAI/USDC, Curve ETHSTETH

raised from 1% on June 19th 2023

Please note that there is still smart contract risk and nothing is truly risk free. NFA

This is subject to change in their coming v4 update.

20m will come from off chain sources in the coming weeks

The market was different pre defi-summer and there was no alternative competition and the number of coins on centralized exchanges for people to purchase was relatively small so the ratios and prices are in a sense inflated and not a great representation. More appropriate to focus on recent price actions like why the ratio went from 1.5 MKR/ETH local high mid 2021 to low of 0.4 MKR/ETH in mid 2023 than why the price dropped from 6 MKR/ETH in the SAI days.

There will be a new name for DAI in V3

The other 30 are given to the workforce bonus pool. This can be topped further with future emissions

People will also be able to generate DAI with the locked up MKR and that DAI can also be used to farm the subDAO tokens in the public yield farm

MKR is planning on launching its own chain

Not counting the private fiat backed ones

Good